The Changing Nature of the $1m+ Art Market

Covid-19 and other historic disruptions to the world’s economy didn’t stop the wealthiest people from buying high-end art, but it changed the way they did so

T he five years from 2018 to 2022 witnessed game-changing global socio-political and economic events: the Covid-19 pandemic; the departure of the UK from the European Union; the rise of nationalist and populist politicians around the globe; heightened tension between China and the West; and the shock invasion of Ukraine by Russia.

Despite these turbulent times, the upper end of the art market has proved remarkably resilient. The London-based art market analysis firm ArtTactic has researched sales of $1m+ works of art at the three major auction houses – Sotheby’s, Christie’s and Phillips – over this period for this report. It found that after a sharp dip from $7.44bn in 2018 to $3.52bn in 2020, the nadir of the pandemic, total $1m+ sales have bounced back vigorously to $8.15bn, a rise of 9.5% between the start of 2018 and the end of 2022.

Covid-19 affected the art market in several ways. Auctions, galleries and art fairs are traditionally social spaces, but the pandemic forced them to pull down their shutters. This heralded efforts to sell art online, a hitherto largely disregarded aspect of the high-end art sales business.

While galleries and fairs largely struggled with online viewing rooms (revenues only really improved when their physical spaces reopened in summer 2021) digital auctions have proved a success, either online-only or hybrid online and livestreamed sales. Research by ArtTactic shows that in 2018 online-only sales at Sotheby’s, Christie’s and Phillips accounted for just $116m; by 2022, this had grown to just under $900m.

The high-end art market can be seen in the context of the larger luxury world. During the pandemic, Bloomberg reported that “the super-rich are buying luxury online like nothing before”, as sales of luxury objects and other collectibles at the top three auction houses boomed. According to ArtTactic, total sales of jewellery and watches at Sotheby’s, Christie’s and Phillips reached $1.62bn in 2022, 19.5% higher than in 2018, while sales of clothing and accessories jumped from $14.4m in 2018 to $122.5m in 2022. The fashion for cross- collecting has been stimulated by the introduction of themed cross-sector auctions of fine art and luxury. In January this year, a LeBron James basketball vest sold for $3.7m as part of a sale including antiquities, fine art and luxury goods, while the number of $1m+ sales of limited-edition sneakers continues to grow.

“While the market for $1m+ art has grown, there have been significant changes in the works that achieve this benchmark”

Technological innovation was behind another significant feature of the five-year period: the rapid rise in sales of digital art and non-fungible tokens (NFTs). Digital art has a half-century history but NFTs are an entirely contemporary phenomenon. Sales of art NFTs grew from almost nothing in January 2021 to $17bn a year later on the leading platforms – OpenSea, NFTX, Larva Labs, LooksRare, SuperRare and Rarible – according to data gathered in 2022 by Bloomberg.

NFTs entered the mainstream art world too: so far, six NFTS have sold for more than $1m, all in 2021, including the record-breaking $69m Everydays:the First 5000 Days by Beeple. Despite their volatility, and the current “crypto winter”, buying cryptocurrency and NFTs has become an essential feature of younger collectors’ spending on digital art.

The worldwide relief at the end of Covid-19 lockdowns is now evident. As confidence about entering public spaces has returned, museums, galleries and biennials are seeing an upsurge in visitors. Last year’s 59th edition of the Venice Biennale, which was postponed from 2021, welcomed 800,000 visitors, a 35% increase on the 2019 exhibition and the highest attendance in its 127-year history. Museums are once more hosting blockbuster art shows – the current Vermeer exhibition at the Rijksmuseum in Amsterdam sold out in just a few days.

The art world as a whole has clearly weathered the storms of the past five years relatively well. But while the market for $1m+ art has grown overall, there have been significant changes in the works that achieve this benchmark, the number of buyers, their motivation, and how they participate.

The rise in the upper end of the art market is related to the rise in global wealth. In 2018, the investment bank Credit Suisse estimated that there were 149,890 people it classifies as “ultra-high-net-worth individuals” (UHNWIs) worldwide. This means they have personal assets, excluding property, worth $50m or more; people who could easily afford to spend $1m or more on art at auction. By 2022, this number had risen to 264,200. The rise in other high-wealth bands was just as marked. It estimated that in 2018, 50,230 individuals were worth more than $100m, and 4,390 more than $500m. By 2022 these numbers had risen to 84,490 and 7,070, respectively.

The US is the richest country by an enormous margin: it has 141,140 UHNWIs, more than half of the world’s total. The US was responsible for much of the global increase in wealth, accounting for 46,000 of new UHNWIs, followed by China, which grew by 19% to 32,710. The Asia-Pacific region’s UHNWIs, excluding China and India, also grew by 14% to 30,010.

“Over the past two decades... the global population of billionaires has risen more than fivefold and the largest fortunes have rocketed past $100bn,” wrote Ruchir Sharma, chair of Rockefeller Capital Management’s international section and Financial Times columnist, in 2021. This has happened because governments, despite growing inflation worldwide and falls in public-sector wages, fear an exodus of the rich, so are reluctant to introduce personal wealth or business taxes.

Meanwhile, a wealthy younger group of individuals is emerging. They are benefiting not only from high incomes in booming sectors such as digital technology, but are also beginning to inherit money and assets from their parents. The so-called Silent Generation (born between 1928 and 1945) and Baby Boomers (born between 1946 and 1964) are in the process of passing on an estimated $30tn–$68tn, in what economists describe as the largest-ever intergenerational wealth transfer.

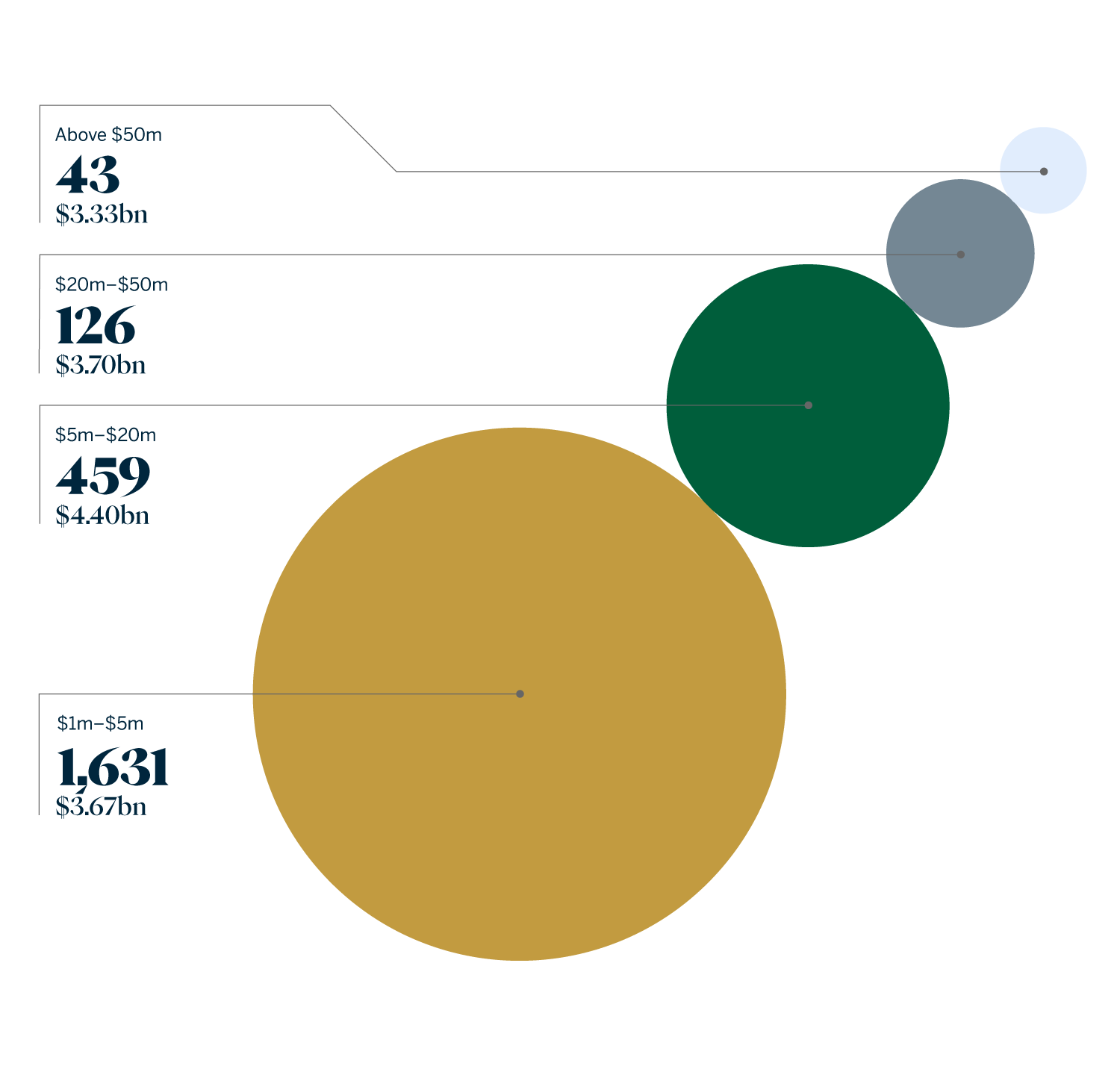

As fortunes have grown, high-end sales of fine art at auction have significantly increased. According to ArtTactic, the value of sales for works over $1m has increased by 9.5%, from a total of $7.44bn in 2018 to $8.15bn in 2022, despite the intervening pandemic. The increase in sales of art over $20m is also marked, rising from $2.67bn to $3.69bn (37.9%) in just five years.

What drives the wealthy to spend substantial sums on art remains surprisingly under-researched. In a recent paper (A Sociological Theory of Contemporary Art Collectors, Routledge, 2021), Fabio Rojas, professor of sociology at Indiana University, notes that while “art collectors have their own motivations... apart from financial investments”, these are poorly understood.

“At one extreme, there are collectors who are actively focused on the more competitive elements of the art world, such as selling art for profit and acquiring works from highly prestigious artists,” Rojas writes. “At the other, there are collectors who are mainly concerned with buying art from people they are friends with, and who are concerned with contributing to the community of artists.” He contrasts these “hierarchy-orientated” and “community-orientated” collectors, but in practice most collectors tend to combine both approaches.

Arguably, it is the unique, hedonic nature of art that makes it so desirable – and more valuable – than other luxury assets such as jewellery and watches. High-end artworks are powerful cultural signifiers, connecting collectors with artists, important public museums, and signalling membership of an elite social group.

Art can also be seen as enabling social agency, giving a voice to previously marginalised artists such as women and people of colour, while collecting ultra-contemporary art can signify philanthropic support for emerging and/or dispossessed communities. Connoisseurial collecting (in-depth collecting) indicates a high level of knowledge and intellectual sophistication. Ironically, the cultural factors that make art so desirable push up its financial value, which in turn attracts buyers who are only interested in it as an investment.

Knight Frank’s The Wealth Report 2022 surveyed more than 600 private bankers, wealth advisers and family offices, which together manage $3.5tn in assets, about the behaviour of their UHNWI clients. It found that there has been a 25% increase on average in “investments of passion” by global UHNWIs, in luxury goods, classic cars, art and wine.

“Arguably, it is the unique, hedonic nature of art that makes it so desirable – and more valuable – than other luxury assets”

The figures are significantly higher in certain regions: Australasia saw a 39% increase; Asia 30%; Latin America 38%; the UK 25% and the Middle East 29%. UHNWIs in all regions except Asia stated that their main reason for passion investments was the “joy of ownership”, while Asians saw them primarily as financial investments. In almost all of the regions surveyed, art was the number one “passion” investment. The only exceptions were Africa, the Middle East and Russia, where art came second after either classic cars or jewellery.

For the annual Art Basel and UBS Global Art Market Report, research firm Arts Economics and UBS Investor Watch surveys collectors who spend at least $10,000 on art and antiques each year. Of 2,339 respondents to the 2022 survey, 88% had bought art, the largest percentage for any luxury category. In 2021, 34% had spent more than $1m on art or antiques, rising to 66% of UHNWIs. Significantly for the future of high-end spending on art – especially Contemporary – 52.5% of the collectors were Millennials (born between 1981 and 1996) and 6.2% were even younger members of Generation Z (born between 1997 and 2012).

Works of art with high cultural value – validated by the presence of similar works in important collections – are scarce. This is creating competition between a growing number of wealthy individuals to buy the best and is driving the upper-end “masterpiece” market.

In 2020, in the depths of the pandemic, only one work sold for more than $50m, Francis Bacon’s 1981 Triptych Inspired by the Oresteia of Aeschylus, which made $84.6m. By 2022, 24 works had sold for more than $50m compared with 15 in 2018, a rise of 60%. The trend is visible across all sectors, especially Impressionist and Modern art. In 2018, 11 works sold for over $50m at auction; by 2022 this had risen to 18 works, a rise of 63.6%.

Commentators have long described the Old Master market as a “masterpiece” market. In 2022, three paintings in this category sold for more than $40m: two works by Renaissance master Botticelli and one by the lesser-known 19th-century history painter Emanuel Leutze. A smaller version of his giant Washington Crossing the Delaware, 1851, which hangs in the Metropolitan Museum of Art, sold for $45m.

Everyone working in the international art world is now aware of an unofficial but powerful rewriting of the artistic canon, signalled in museums such as Tate Modern in London and the Museum of Modern Art in New York by extensive rehangs of their Modern and Contemporary collections. These now include far more works by women, artists of colour, artists from outside the North American and Western European hegemony and those representing LGBTQ+ perspectives.

Similar trends are now observable at the very top end of the auction market. Works by women artists accounted for a quarter of the Contemporary works sold at auction in 2022, double the number in 2018. African American artists, including Stanley Whitney, Rashid Johnson and Simone Leigh, are also moving up the rankings.

The people bidding at auctions are also changing. Sotheby’s provided ArtTactic with previously unpublished data about bidders for this report. While North Americans were unsurprisingly the biggest group (45%), followed by Europeans (32%), the number of Asians bidding jumped by 40% between 2018 and 2022, and they accounted for 18% of $1m+ Contemporary art bids last year. Bidders are also getting younger: Millennials accounted for almost a fifth (17%) of Contemporary art bids over $1m.

It is a well-known adage that past performance is no guarantee of future results. While less dire than the predictions at the end of 2022, the global economic outlook is still uncertain. The International Monetary Fund’s latest projection is for sluggish growth in 2023 and 2024: “The rise of central bank rates to fight inflation and Russia’s war in Ukraine continue to weigh on economic activity,” it warns, and the balance of risks “remains tilted to the downside”.

Nevertheless, as was seen after the financial crisis of 2008–09, the upper end of the art market has demonstrated strong resilience in the face of financial downturns. Can it weather the “permacrisis” – Collins Dictionary’s telling 2022 Word of the Year?

The latest Euromonitor International Global Wealth and Luxury Report forecasts that the number of people in its three wealthiest categories – UHNWIs, high-net-worth individuals (HNWIs) and “affluent consumers” – will rise by 65.5% by 2030, based on an estimated 3.6% average growth in global GDP, led by India and China.

The top five countries by number of UHNWIs in 2030 are predicted to be the US, China, Germany, the UK and Canada. The equivalent HNWI chart is topped by the US, China, Germany, the UK and France. These countries are expected to double their number of UHNWIs and HNWIs over the next 10 years. All of these countries have established art markets.

Meanwhile, the gender pay gap is set to narrow further. “While women are often decision-makers when it comes to household purchases, their rising pay will increase their role in luxury/big ticket item markets,” says the Euromonitor report. The top five countries for female disposable income by 2040 are predicted to be the US, China, Switzerland, Norway and Australia, which bodes well for their art markets and the cultural and financial rankings of women artists, who are often supported by female collectors.

“The upper end of the art market has demonstrated strong resilience in the face of financial downturns”

Geographically, the Asia-Pacific region is set to become “the world’s largest consumer market” and Asian consumers will be “the key trend-setters, shaping global demand for consumer goods and services”. Current data suggests that Asian bidders, at least for the foreseeable future, are most likely to follow western art market trends.

Demographically, Millennials will be the most affluent consumers by 2040, “creating consumer demand for higher value goods... looking for comfort in their homes and meaningful experiences outside of them”.

As well as seeking emotional and intellectual stimulation, younger buyers are also more investment-minded. A survey by Bank of America in 2022, Private Bank Study of Wealthy Americans, found that alternative assets such as art are growing in appeal down the generations. Only 5% of HNWIs aged over 43 said they would add alternative investments such as art to their portfolios, but this trebled to more than 16% of people aged 21 to 42, and the trend is likely to continue.

In 2017, the art world was stunned by the sale at auction of Leonardo da Vinci’s Salvator Mundi for a record-breaking $450.3m, making it the most expensive artwork ever sold. It remains an outlier: between 2018 and 2022 only 10 works of art broke the $100m threshold, while none sold for more than $200m at auction.

Nevertheless, while governments remain unwilling to restructure tax regimes, the disposable incomes of the rich will continue to rise. As long as younger generations regard art as an important signifier of lifestyle, community action and philanthropy (as well as a canny investment), and older wealthy individuals as a marker of status and acquired knowledge, the $1m+ art market is surely set to grow.